Mortgages Fundamentals Explained

Table of ContentsSome Ideas on Team Quintez - Integrity Home Mortgage Corporation You Should KnowNot known Details About Mortgage Lender 5 Simple Techniques For Mortgage LenderThe Ultimate Guide To Buy A Home

15-year finances were more economical at 4. 06%. ARMs were even more affordable, with prices as low as 3. 13% offered. Our rate tables are upgraded day-to-day as well as will certainly show you the most up to date prices for your area. There are four core components of a mortgage repayment: the principal, interest, tax obligations, and also insurance policy, jointly referred to as "PITI." There can be other expenses included in the repayment.

If you were to purchase a $100,000 home, as an example, and obtain $90,000 from a loan provider to help spend for it, that 'd be the principal you owe. The interest, revealed as a percent rate, is what the lender fees you to borrow that cash. To put it simply, the rate of interest is the yearly price you pay for borrowing the principal.

The home mortgage's promissory note is what actually represents the loan. One more crucial factor: While a mortgage is protected by actual residential or commercial property (in other words, your house), various other types of loans, such as credit report cards, are unsafe, states Jodi Hall, head of state of Nationwide Home mortgage Bankers, Inc., in Melville, New York.

6 Simple Techniques For Buy A Home

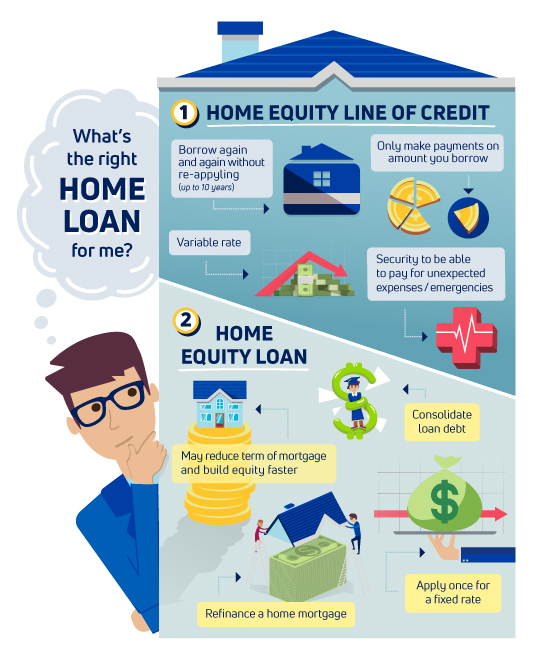

If the home were to be confiscated as well as the lending institution markets the property, the proceeds of the sale would initially approach paying back the first mortgage, because it's in the senior lien position. A 2nd home mortgage describes a lien in a jr placement, such as a house equity line of credit (HELOC) or house equity loan.

Aim to make every one of your charge card, funding or various other financial obligation payments on schedule, and check your credit history records for any type of errors prior to looking for a home loan. If you detect incorrect information (like wrong call details), dispute it with the credit rating reporting bureau as quickly as possible to get it corrected.

As you weigh your home loan choices, right here are some basic terms you may come across (and also below are other essential terms to recognize). Amortization explains the procedure of repaying a finance, such as a home mortgage, in installment payments over a time period. Component of each repayment goes toward the principal, or the amount obtained, while the other part goes toward passion (Mortgage Lender).

, shows the price of obtaining the money for a home mortgage. A broader procedure than the interest price alone, the APR includes the interest rate, discount rate factors as well as various other fees that come with the loan.

The Single Strategy To Use For Loan For Home

Buyers commonly place down a percent of the residence's worth as the down repayment, after that obtain the remainder in the kind of a home loan. A larger down payment can aid boost a borrower's possibilities of getting a lower passion rate.

An escrow account holds the part of a debtor's monthly mortgage payment that covers homeowners insurance costs as well as building taxes. Escrow accounts additionally hold the down payment the purchaser deposits between the time their offer has actually been accepted and the closing. try here An escrow make up insurance and also tax obligations is typically established up by the mortgage lending institution, that makes the insurance and also tax payments on the debtor's part.

The servicer accumulates your repayments and, if you have an escrow account, makes sure that your tax obligations as well as insurance coverage are paid on time. The servicer also steps in with relief choices if you're having difficulty making repayments.

A home mortgage is likely to be the biggest, longest-term car loan you'll ever get to acquire the largest possession you'll ever before have your home - loan for home. The more you understand how a home mortgage works, the much better furnished you need to be to choose the mortgage that's right for you. A mortgage is a financing you obtain from a loan provider to finance a home acquisition.

The Single Strategy To Use For Team Quintez - Integrity Home Mortgage Corporation

Below are some usual terms you'll need to understand if you're obtaining a home loan: The cosigned promissory note, or "note" as it is much more typically labeled, outlines just how you will certainly pay off the financing, with details consisting of: Your rate of interest rate Your overall loan amount The term of the funding (thirty years or 15 years are usual examples) When the financing is taken this into consideration late Your regular monthly principal as well as rate of interest repayment.

The home mortgage offers the loan provider find out here now the right to take ownership of your residence as well as market it if you don't make payments at the terms you consented to on the note. An act of trust jobs like a mortgage and also is protected versus your residence. Most home mortgages are agreements between two parties you and the lender.

A deed of count on offers the trustee the authority to take control of your residence in behalf of the loan provider if you stop making repayments. These are expenditures billed by a lending institution to make or stem your loan. They generally include origination charges, discount rate factors, costs associated with underwriting, handling, document prep work as well as financing of your car loan.

While charges differ extensively by the type of home mortgage you obtain and by location, they usually total 2% to 6% of the lending amount. On a $250,000 mortgage, your closing expenses would certainly amount to anywhere from $5,000 to $15,000.